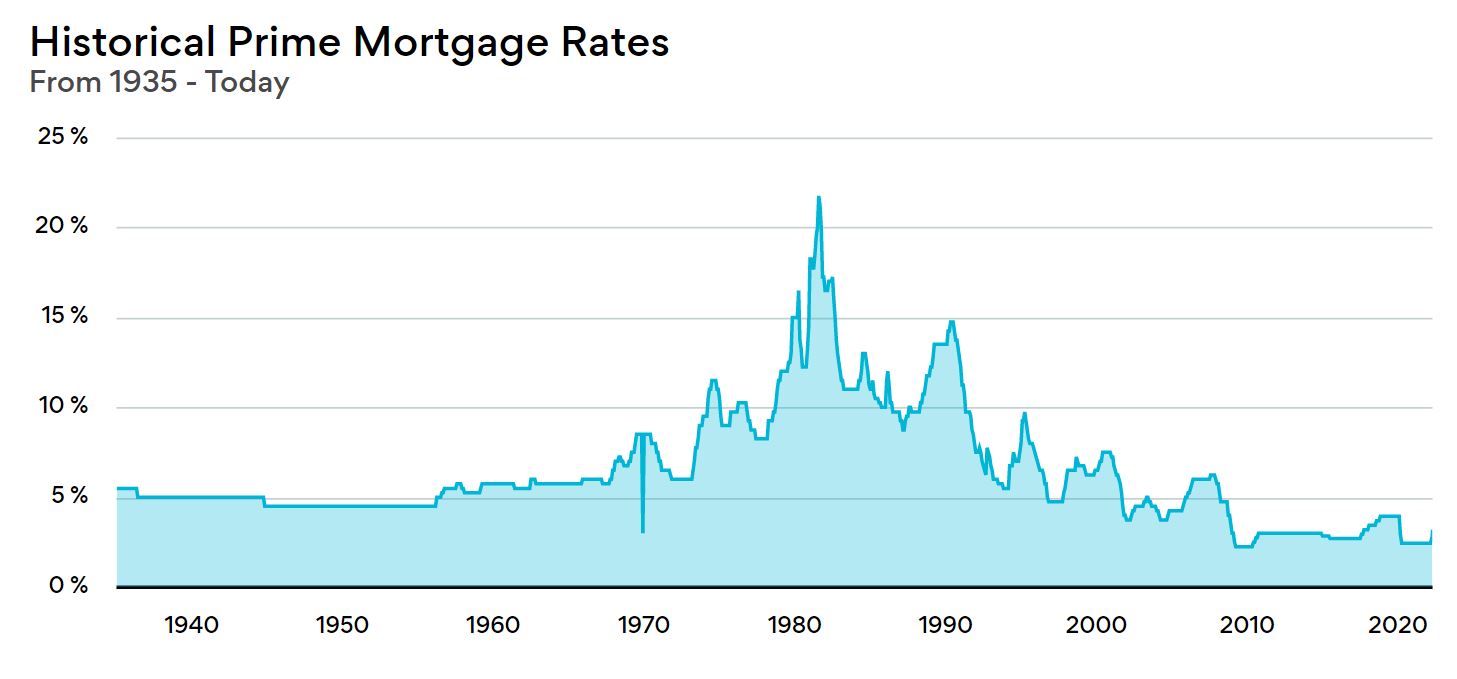

Prime Mortgage Rate is the interest rate at which banks lend to their most creditworthy customers. It is one of the most important factors in the home loan process and can make a big difference in your monthly payments. To help you understand prime mortgage rate, this post will explain what it is and how it works, along with common terms like LIBOR and Fed Funds Rate.

Prime Mortgage Rate is the interest rate at which banks lend to their most creditworthy customers. It is one of the most important factors in the home loan process and can make a big difference in your monthly payments. To help you understand prime mortgage rate, this post will explain what it is and how it works, along with common terms like LIBOR and Fed Funds Rate.

Breaking Down ‘Prime Mortgage Rate’

The prime mortgage rate (also called the “prime lending rate”) is an interest rate that banks use to determine how much to loan their most creditworthy customers. It’s typically higher than the federal funds rate, which acts as a general benchmark for all other rates charged by banks on loans and is controlled by the Federal Reserve Bank.

How Prime Mortgage Rates Work

The prime mortgage rate is the benchmark for all other mortgage rates. It’s generally the lowest rate that a bank will offer to its most creditworthy customers. Because banks use this rate as the base for their loans, it directly affects other types of borrowing from them, such as home equity lines of credit (HELOCs). The government sets the initial prime rate each year, but it may change during any month if economic conditions warrant it.

The Difference Between Prime Mortgage Rate and LIBOR

If you’re not familiar with how LIBOR works, let’s first understand what it is. The London Interbank Offered Rate (LIBOR) is the benchmark interest rate at which banks lend to each other. It’s also used as a benchmark for many other rates, such as mortgages and student loans. Essentially, banks use LIBOR as a basis for determining their own interest rates on loans and credit cards; in doing so, they hope to make more money than the rate at which they have borrowed from each other.

Prime Mortgage Rate and Fed Funds Rate

The TD Prime Mortgage Rate is a benchmark used to set the interest rates on mortgages, auto loans and other consumer loans. It’s also known as the prime rate and is used by banks to determine their own lending rates. The Federal Open Market Committee (FOMC) sets monetary policy for the U.S., while the Fed Funds Rate (or fed funds rate) is used to control inflation and stabilize economic growth by adjusting how much money banks lend each other overnight during times of financial stress.

No, you don’t need to be a Bond villain to get one. The prime rate is the interest rate at which banks lend money to those who own homes and have good payment history. It’s used as an indicator for other interest rates such as variable-rate mortgages, car loans and credit cards. The prime rate will usually increase when the economy is doing well because people are more likely to borrow more money at higher rates when they feel confident in their financial situation. As you can see, there are a lot of factors that go into determining the prime mortgage rate. It’s important for homeowners and potential homebuyers to understand what their options are when looking at mortgage rates. If you’re wondering whether or not it’s time for you to refinance your home loan, we’d love to help! Contact us today so we can discuss how our services could benefit your financial situation.